What does "average tax return for $40,000 income" mean?

The average tax return for a $40,000 income can vary depending on a number of factors, including filing status, deductions, and credits. However, according to the IRS, the average tax refund for a single filer with no dependents who earned $40,000 in 2022 was $2,800. The average refund for a married couple filing jointly with no dependents who earned $40,000 was $5,600.

There are a number of things that can affect the size of your tax refund, including:

- Your filing status

- Your income

- Your deductions

- Your credits

If you want to increase the size of your tax refund, there are a number of things you can do, including:

- Make sure you are claiming all of the deductions and credits that you are eligible for.

- Contribute to a retirement account, such as a 401(k) or IRA.

- Itemize your deductions instead of taking the standard deduction.

You can also use a tax refund calculator to estimate the size of your refund before you file your taxes.

It is important to note that the average tax refund is just that - an average. Your actual refund may be more or less than the average, depending on your individual circumstances.

- Lebron James Father

- Wentworth Miller Wife And Kids

- Christieides Wife

- Prichard Colon

- Is Tulsi Gabbard Married With Children

Average Tax Return for $40,000 Income

The average tax return for a $40,000 income can vary depending on a number of factors, but there are some key aspects that can help you understand the topic better:

- Filing status: Your filing status can affect the size of your tax refund. For example, single filers typically receive a smaller refund than married couples filing jointly.

- Income: Your income is another important factor that can affect the size of your tax refund. The more you earn, the more taxes you will owe, and the smaller your refund will be.

- Deductions: Deductions can reduce your taxable income, which can lead to a larger tax refund. Some common deductions include mortgage interest, charitable contributions, and state and local taxes.

- Credits: Credits can also reduce your tax liability, which can lead to a larger tax refund. Some common credits include the child tax credit, the earned income tax credit, and the saver's credit.

- Withholding: The amount of tax that is withheld from your paycheck can also affect the size of your tax refund. If too much tax is withheld, you will receive a larger refund. If too little tax is withheld, you may owe money when you file your taxes.

- Estimated taxes: If you are self-employed or have other income that is not subject to withholding, you may need to make estimated tax payments. These payments can help you avoid owing money when you file your taxes and can also lead to a larger tax refund.

By understanding these key aspects, you can take steps to increase the size of your tax refund. For example, you can make sure that you are claiming all of the deductions and credits that you are eligible for, and you can adjust your withholding so that the right amount of tax is being taken out of your paycheck.

The filing status of a taxpayer can significantly impact the average tax return for a $40,000 income. Single filers typically receive a smaller refund than married couples filing jointly. This is because married couples are able to combine their incomes and deductions, which can result in a lower overall tax liability. Additionally, married couples may be eligible for certain tax credits and deductions that are not available to single filers.

For example, the standard deduction for married couples filing jointly in 2023 is $27,700, while the standard deduction for single filers is only $13,850. This means that married couples can deduct more of their income from their taxable income, which can lead to a larger tax refund.

In addition, married couples may be eligible for the child tax credit, which is a tax credit of up to $2,000 per qualifying child. This credit is not available to single filers. As a result of these factors, married couples filing jointly typically receive a larger tax refund than single filers with the same income.

Therefore, it is important to consider your filing status when estimating your tax refund. If you are married, you may be able to increase the size of your refund by filing jointly with your spouse.

1. Income

The amount of income you earn is a major factor in determining the size of your tax refund. The more you earn, the more taxes you will owe, and the smaller your refund will be. This is because the tax system is progressive, which means that higher earners pay a higher percentage of their income in taxes.

- Tax Brackets

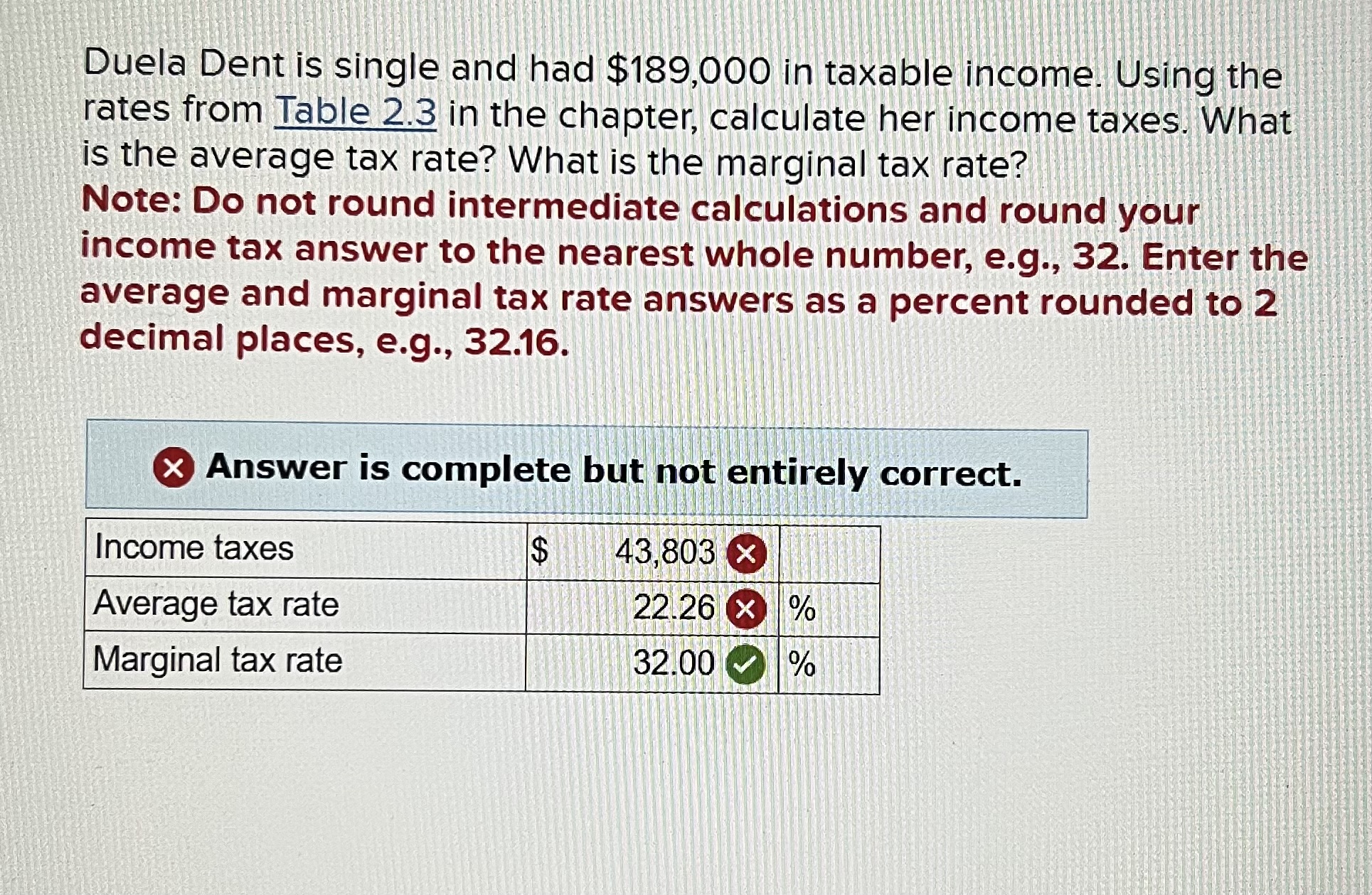

The tax system is divided into tax brackets, which are ranges of income that are taxed at different rates. The higher your income, the higher the tax bracket you will fall into, and the more taxes you will owe. For example, in 2023, the first tax bracket for single filers is 10%, and it applies to income up to $10,275. The second tax bracket is 12%, and it applies to income between $10,275 and $41,775. The third tax bracket is 22%, and it applies to income between $41,775 and $89,075.

- Standard Deduction

The standard deduction is a specific amount of income that you can deduct from your taxable income before you calculate your taxes. The standard deduction varies depending on your filing status. For example, in 2023, the standard deduction for single filers is $13,850. The standard deduction for married couples filing jointly is $27,700. The higher your income, the less your standard deduction will be worth. This is because the standard deduction is phased out for higher earners.

- Itemized Deductions

Itemized deductions are specific expenses that you can deduct from your taxable income. Some common itemized deductions include mortgage interest, charitable contributions, and state and local taxes. Itemized deductions can be more valuable than the standard deduction for higher earners. However, you can only itemize your deductions if they exceed the standard deduction.

- Tax Credits

Tax credits are dollar-for-dollar reductions in your tax liability. Unlike deductions, which reduce your taxable income, tax credits directly reduce the amount of taxes you owe. Some common tax credits include the child tax credit, the earned income tax credit, and the saver's credit. Tax credits can be especially valuable for lower earners.

By understanding how your income affects your taxes, you can make informed decisions about your finances. For example, if you are expecting a large tax refund, you may want to adjust your withholding so that more of your paycheck is taken home. Alternatively, if you are expecting to owe money when you file your taxes, you may want to increase your withholding so that you avoid owing a large amount of taxes at the end of the year.

2. Deductions

Deductions are an important part of the tax system. They allow you to reduce your taxable income, which can lead to a larger tax refund. There are many different types of deductions available, and the ones you can claim will depend on your individual circumstances.

- Mortgage interest

If you own a home, you may be able to deduct the interest you pay on your mortgage. This deduction can be very valuable, especially if you have a large mortgage. To claim this deduction, you must itemize your deductions on your tax return.

- Charitable contributions

You may be able to deduct charitable contributions you make to qualified organizations. This deduction can be especially valuable if you make large donations to charity. To claim this deduction, you must itemize your deductions on your tax return.

- State and local taxes

You may be able to deduct state and local income taxes, as well as property taxes. This deduction can be especially valuable if you live in a state with high taxes. To claim this deduction, you must itemize your deductions on your tax return.

In addition to these common deductions, there are many other deductions that you may be able to claim. To find out what deductions you can claim, consult with a tax professional or refer to the IRS website.

Claiming deductions can help you reduce your taxable income and increase your tax refund. However, it is important to note that deductions are not the same as tax credits. Tax credits directly reduce your tax liability, while deductions reduce your taxable income. As a result, deductions are generally more valuable for higher earners.

3. Credits

Understanding how credits affect the average tax return for $40,000 income is very important to maximizing your refund. Credits are dollar-for-dollar reductions in your tax liability, meaning they can directly increase the size of your refund. Unlike deductions, which reduce your taxable income, credits are applied after your income has been taxed.

The child tax credit is a valuable credit for families with children. The credit is worth up to $2,000 per qualifying child. To claim the child tax credit, you must meet certain income requirements. The earned income tax credit is another valuable credit for low- and moderate-income workers. The credit is worth up to $6,935 for the 2023 tax year. To claim the earned income tax credit, you must meet certain income requirements and have earned income from working.

The saver's credit is a credit for low- and moderate-income taxpayers who save for retirement. The credit is worth up to $1,000 per year. To claim the saver's credit, you must meet certain income requirements and contribute to a qualified retirement account.

Claiming credits can significantly increase the size of your tax refund. By understanding which credits you are eligible for, you can take advantage of these valuable tax breaks.

4. Withholding

The amount of tax that is withheld from your paycheck can also affect the size of your tax refund. If too much tax is withheld, you will receive a larger refund. If too little tax is withheld, you may owe money when you file your taxes. This is because the amount of tax that is withheld from your paycheck is based on your estimated tax liability. If your estimated tax liability is too high, you will have too much tax withheld from your paycheck. If your estimated tax liability is too low, you will not have enough tax withheld from your paycheck.

- Facet 1: How withholding affects your tax refund

The amount of tax that is withheld from your paycheck can have a significant impact on the size of your tax refund. If too much tax is withheld, you will receive a larger refund. If too little tax is withheld, you may owe money when you file your taxes.

- Facet 2: How to adjust your withholding

You can adjust your withholding by completing a new Form W-4 and submitting it to your employer. The Form W-4 will help your employer determine how much tax to withhold from your paycheck.

- Facet 3: The importance of accurate withholding

It is important to make sure that your withholding is accurate. If your withholding is too high, you will have too much tax withheld from your paycheck and you will receive a smaller refund. If your withholding is too low, you may not have enough tax withheld from your paycheck and you may owe money when you file your taxes.

Withholding is an important part of the tax system. By understanding how withholding works, you can make sure that the right amount of tax is withheld from your paycheck. This will help you avoid getting a large tax refund or owing money when you file your taxes.

5. Estimated taxes

"Estimated taxes" are payments made to the IRS throughout the year by individuals who are self-employed or have other income that is not subject to withholding. This includes income from self-employment, freelance work, investments, and rental properties. Estimated tax payments are due four times per year: April 15, June 15, September 15, and January 15 of the following year.

Making estimated tax payments can help you avoid owing money when you file your taxes. This is because estimated tax payments are applied to your tax liability for the year. If you do not make estimated tax payments, you may have to pay a penalty when you file your taxes.

Estimated tax payments can also lead to a larger tax refund. This is because estimated tax payments are refunded to you when you file your taxes. If you overpay your estimated taxes, you will receive a refund for the overpayment.

If you are self-employed or have other income that is not subject to withholding, it is important to make estimated tax payments. Estimated tax payments can help you avoid owing money when you file your taxes and can also lead to a larger tax refund.

FAQs on "Average Tax Return for $40,000 Income"

This section addresses frequently asked questions (FAQs) about the average tax return for individuals with an income of $40,000. These FAQs aim to clarify common concerns and misconceptions, providing concise and informative answers based on relevant tax regulations and guidelines.

Question 1: What is the average tax return for a $40,000 income?

The average tax return for a $40,000 income can vary depending on several factors, including filing status, deductions, and tax credits claimed. According to the Internal Revenue Service (IRS), the average tax refund for single filers with no dependents earning $40,000 in 2022 was approximately $2,800. For married couples filing jointly with no dependents and earning the same income, the average refund was around $5,600.

Question 2: What factors affect the size of my tax return?

The size of your tax return is influenced by various factors, including your filing status, income level, deductions, and tax credits. Filing status, such as single, married filing jointly, or head of household, can impact the tax brackets and standard deduction you qualify for. Your income level determines the tax bracket you fall into, affecting the percentage of your income subject to taxation. Deductions, such as mortgage interest, charitable contributions, and state and local taxes, reduce your taxable income, potentially leading to a larger refund. Tax credits, such as the child tax credit or earned income tax credit, provide direct reductions in your tax liability, further increasing your refund amount.

Question 3: How can I increase the size of my tax refund?

To maximize the size of your tax refund, consider the following strategies: Ensure you claim all eligible deductions and credits. Explore retirement savings options like 401(k) or IRA contributions, which offer tax-deferred growth and potential tax savings. If you itemize deductions, keep track of expenses throughout the year to maximize your deductions. Review your withholding status and adjust it if necessary to ensure the appropriate amount of tax is withheld from your paychecks.

Question 4: What is the difference between a deduction and a tax credit?

Deductions reduce your taxable income, while tax credits directly reduce your tax liability. Deductions lower the amount of income subject to taxation, potentially resulting in a smaller tax bill. Tax credits provide dollar-for-dollar reductions in the taxes you owe, offering a more substantial benefit, especially for low- and moderate-income taxpayers.

Question 5: How can I estimate my tax refund before filing my taxes?

You can estimate your tax refund using online tax calculators or software. These tools consider your income, filing status, and other relevant information to provide an approximate refund amount. Keep in mind that these estimates are not exact and may vary from your actual refund when you file your tax return.

Understanding these key aspects of tax returns can help you navigate the tax filing process effectively. By considering the factors that influence your refund amount and taking proactive steps to optimize your deductions and credits, you can potentially increase your tax refund and maximize your financial well-being.

It is crucial to consult with a tax professional or refer to official IRS resources for personalized advice and to stay up-to-date with the latest tax regulations and changes.

Conclusion

In summary, the average tax return for individuals earning $40,000 can vary depending on several factors, including filing status, deductions, and tax credits claimed. It is important to understand these factors and their impact on your tax return to maximize your refund and minimize your tax liability.

By claiming eligible deductions and credits, exploring retirement savings options, and reviewing your withholding status, you can potentially increase the size of your tax refund. Additionally, utilizing online tax calculators or consulting with a tax professional can provide valuable insights and help you navigate the tax filing process effectively.

Understanding the nuances of tax returns empowers you to make informed decisions, optimize your financial situation, and fulfill your tax obligations accurately. Stay informed about the latest tax regulations and seek professional guidance when needed to ensure compliance and maximize your tax benefits.

- Trey Gowdy Nose Before And After

- Seanuffyalary At Fox

- Perdita Weeksisability

- Jackerman

- Gerard Butler Relationship